Retirees are people who have stopped working full time after years in the workforce. Most are over 60 and rely on a mix of Social Security benefits, retirement savings, and sometimes part time work to cover their living expenses. You might be getting ready to retire, already retired, or helping a loved one navigate this transition. Either way, understanding your options matters more than ever.

This guide breaks down everything you need to know about retirement benefits and resources. You’ll learn how to maximize your Social Security payments, manage your healthcare coverage through Medicare or other options, handle taxes on withdrawals from retirement accounts, and even find ways to earn extra income if you want or need it. We cover the money decisions that affect your daily life, the government programs designed to help you, and practical strategies for making your retirement years work financially. By the end, you’ll have a clear picture of what’s available and how to access it.

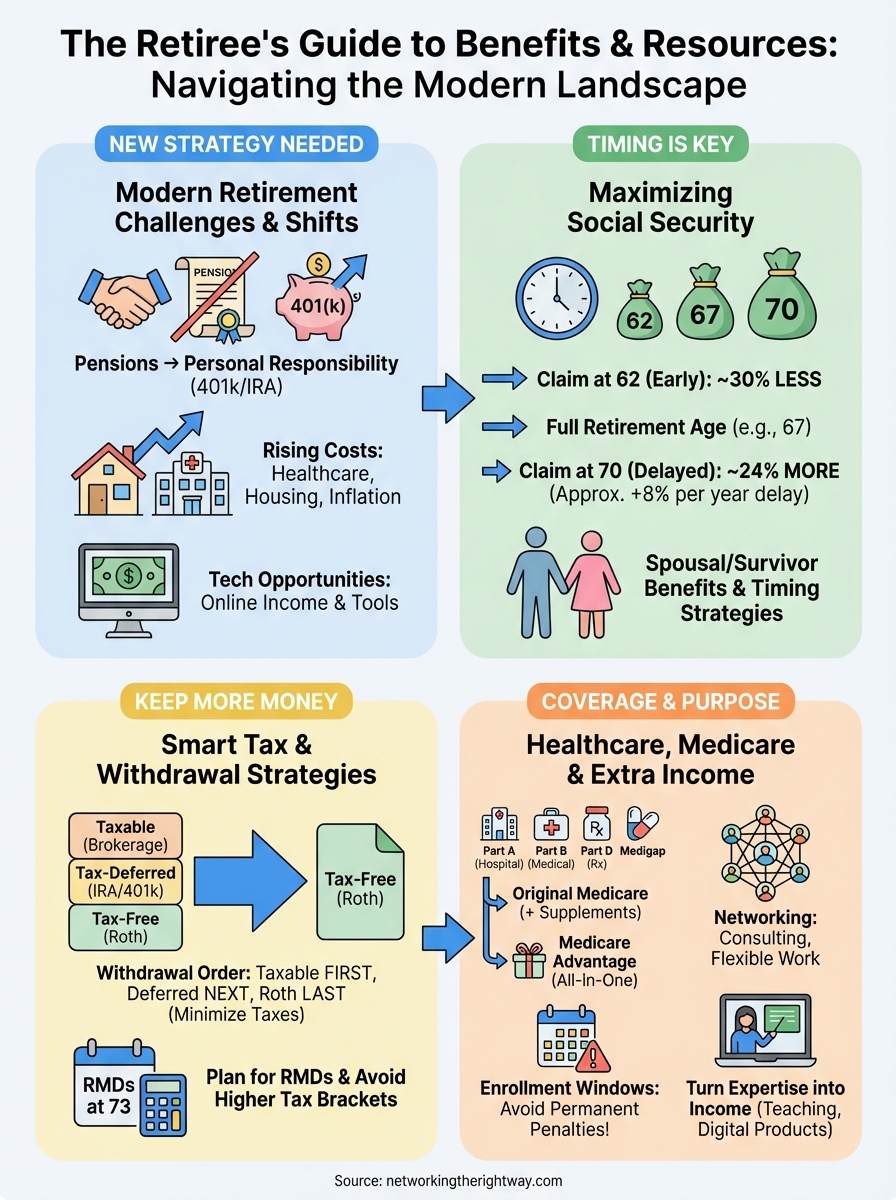

Why modern retirement demands a new strategy

Your parents’ retirement playbook doesn’t work anymore. The traditional model relied on company pensions, Social Security, and maybe some modest savings to get you through your golden years. Today’s reality looks completely different. Most companies stopped offering pension plans decades ago, Social Security replaces less of your income than it used to, and you’re expected to live 20 or 30 years after leaving the workforce. These changes mean you need to think about retirement differently than previous generations did.

The shift from pensions to personal responsibility

Workplace retirement benefits changed dramatically starting in the 1980s. Companies replaced guaranteed pension payments with 401(k) plans that put the investment risk on your shoulders instead of theirs. You now decide how much to save, where to invest it, and when to withdraw it. Only about 15% of private sector workers still have traditional pension plans, compared to over 60% in the early 1980s. This shift transferred all the responsibility to you, and many people approaching retirement today didn’t save enough early in their careers because they didn’t fully understand this change.

Rising costs outpace traditional planning

Healthcare expenses alone can derail even careful retirement plans. The average couple retiring today needs roughly $315,000 just to cover medical costs throughout retirement, and that figure doesn’t include long-term care. Housing costs keep climbing in most areas, property taxes increase, and inflation erodes your purchasing power every year. Your Social Security payments get cost of living adjustments, but they often lag behind real increases in what you actually spend money on.

The gap between what retirees need and what they have saved continues to widen every year.

Long-term care presents another massive expense that wasn’t part of earlier retirement calculations. A nursing home can cost $100,000 per year or more, and Medicare doesn’t cover most of these costs. Half of people over 65 will need some form of long-term care, yet most have no plan to pay for it.

Technology changes the game

The internet opened new possibilities that didn’t exist for previous generations of retirees. You can now earn supplemental income from home through online work, consulting, or digital products. You can manage your investments directly without paying high fees to traditional advisors. You can research healthcare options, compare prescription drug prices, and access free educational resources that help you make better financial decisions. These tools give you more control, but they also require you to learn new skills and stay engaged with technology rather than simply coasting through retirement.

How to maximize your guaranteed government benefits

Social Security forms the foundation of most retirement income, but you get to decide when and how to claim it. Your choices directly impact how much money you receive every month for the rest of your life. Most retirees leave thousands of dollars on the table by claiming benefits too early or without understanding their options. The government offers several programs designed to support you, and learning how to use them correctly makes a significant difference in your financial security.

Understanding your Social Security timing options

You can start collecting Social Security as early as age 62, but waiting longer increases your monthly payment substantially. If you claim at 62, you receive about 30% less than you would at your full retirement age of 67. Wait until 70, and you get roughly 24% more than at 67. Each year you delay between full retirement age and 70 adds approximately 8% to your benefit. This increase is permanent and applies to every payment you receive for life.

Delaying Social Security is the closest thing to a guaranteed investment return you’ll find anywhere.

Your health, life expectancy, and need for income all factor into this decision. Someone in poor health might benefit from claiming early, while someone in excellent health with other income sources gains more by waiting.

Claiming strategies that increase your monthly check

Married couples have additional options that single people don’t. If one spouse earned significantly more than the other, the lower earner can claim spousal benefits worth up to 50% of the higher earner’s benefit. Divorced individuals married for at least 10 years can claim based on their ex-spouse’s record without affecting what the ex-spouse receives. Widows and widowers can switch between survivor benefits and their own retirement benefit, letting them claim the lower amount first and switch to the higher one later. Check your earnings record on the Social Security website every few years to catch mistakes before they permanently reduce your benefits.

How to manage taxes and income withdrawals

Your retirement accounts come with tax rules that affect how much money you actually get to spend. The government requires you to start taking required minimum distributions (RMDs) from traditional IRAs and 401(k)s at age 73, and you pay ordinary income tax on every dollar you withdraw. Pull out too much in one year, and you could push yourself into a higher tax bracket or trigger taxes on your Social Security benefits. Smart withdrawal planning keeps more money in your pocket instead of sending it to the IRS.

Creating a tax-efficient withdrawal sequence

You control your tax bill by choosing which accounts to tap first. Most retirees benefit from withdrawing money from taxable brokerage accounts before touching tax-deferred accounts like traditional IRAs. This strategy lets your retirement accounts keep growing tax-free for as long as possible. Roth IRA withdrawals come out completely tax-free, so save those for last or use them strategically in years when you need extra cash without triggering higher taxes. Some years you might want to convert portions of a traditional IRA to a Roth IRA when your income drops temporarily, locking in a lower tax rate on that money forever.

The order you withdraw from different account types determines how much you pay in taxes over your entire retirement.

Avoiding common withdrawal mistakes

Many people withdraw the same amount every year regardless of their tax situation or actual needs. This approach often wastes opportunities to minimize taxes. You might withdraw less in years when you have other taxable income from part-time work or selling assets, then take larger distributions in low-income years. Watch for the thresholds where Social Security becomes taxable (combined income over $25,000 for singles or $32,000 for married couples). Taking just a few thousand dollars less can sometimes save you from taxes on your benefits. Calculate your withdrawals each year based on your total tax picture, not just what you think you need to spend.

Finding the right healthcare coverage options

Healthcare becomes your single largest expense category in retirement. Medicare covers most retirees starting at age 65, but the program splits into multiple parts with different costs and coverage rules. You face enrollment deadlines that carry lifetime penalties if you miss them, and you need to choose between traditional Medicare with separate drug coverage or all-in-one Medicare Advantage plans. Understanding these options before you need them prevents expensive mistakes and coverage gaps that leave you paying for medical care out of pocket.

Understanding your Medicare enrollment windows

You get a seven-month window to sign up for Medicare that starts three months before you turn 65, includes your birthday month, and extends three months after. Miss this window, and you pay a permanent penalty added to your Part B premium for as long as you have Medicare. The penalty equals 10% of the standard premium for each 12-month period you were eligible but didn’t enroll. If you’re still working past 65 with employer coverage of 20 or more employees, you qualify for a special enrollment period that lets you delay Medicare without penalties. Track these dates carefully because the government won’t remind you, and fixing enrollment mistakes takes months of waiting.

Choosing between original Medicare and Medicare Advantage

Original Medicare gives you Part A (hospital coverage) and Part B (doctor visits and outpatient care), but you need to add Part D for prescriptions and either a Medigap supplement or pay 20% of costs yourself. Medicare Advantage plans bundle everything into one plan, often including extras like dental and vision, but they limit you to specific networks of doctors and hospitals. Compare the total annual costs including premiums, deductibles, and maximum out-of-pocket limits for both options based on your actual healthcare needs.

Your choice between Medicare types locks you in for at least a year, so evaluate carefully before deciding.

Finding purpose and extra income through networking

Retirement doesn’t mean you stop contributing or earning. Many retirees find that staying connected to professional networks brings both financial benefits and personal fulfillment. You built valuable skills and relationships over decades of work, and these connections remain assets you can leverage. Networking in retirement looks different than climbing the corporate ladder, but it opens doors to consulting opportunities, part-time roles, mentorship positions, and collaborative projects that fit your schedule and interests.

Building connections that lead to paid opportunities

Your former colleagues, industry contacts, and professional acquaintances form a ready-made network for finding flexible work. Reach out to people you worked with to let them know you’re available for consulting or project-based work. Companies often prefer hiring experienced retirees as contractors because they get expertise without long-term commitments. You bring institutional knowledge that younger workers lack, and businesses will pay for that insight. Join online platforms where professionals in your field gather, participate in discussions, and share your expertise. LinkedIn remains the primary professional network where you can signal your availability and skills.

Former employers and industry contacts already trust your work, making them your best source for paid opportunities.

Turning expertise into income streams

Your decades of experience translate directly into teaching and coaching opportunities. Local community colleges, adult education programs, and online course platforms need instructors with real-world knowledge. You can create digital courses once and sell them repeatedly, or offer one-on-one coaching sessions to people entering your former field. Writing articles, speaking at industry events, and serving on advisory boards all generate income while keeping you engaged with your profession. These activities typically pay $50 to $200 per hour or more depending on your expertise level, and you control exactly how much time you invest.

Rethinking your next chapter

Your retirement success depends on taking action now rather than hoping things work out. You’ve learned how to maximize Social Security benefits, manage your withdrawals to minimize taxes, navigate healthcare options, and leverage your network for extra income. These strategies work only when you actually implement them, not when they sit as good ideas you’ll get to someday. Most retirees who struggle financially made the mistake of waiting too long to plan or assuming their situation would somehow fix itself.

Start with one area where you need the most help, whether that’s understanding your Medicare options or figuring out when to claim Social Security. Then move to the next priority on your list. If you want to earn supplemental income online but feel overwhelmed by the technology, consider a simple way to build a business online designed specifically for people over 50 who lack tech skills. Your next chapter can provide both financial security and personal satisfaction when you approach it with the right information and take concrete steps forward.